code

share

In this post we formally describe the problem of linear regression, or the fitting of a representative line (or hyperplane in higher dimensions) to a set of input/output data points. Regression in general may be performed for a variety of reasons: to produce a so-called trend line (or - more generally - a curve) that can be used to help visually summarize, drive home a particular point about the data under study, or to learn a model so that precise predictions can be made regarding output values in the future.

# imports from custom library

import sys

sys.path.append('../../')

import matplotlib.pyplot as plt

from mlrefined_libraries import superlearn_library as superlearn

import autograd.numpy as np

import math

import pandas as pd

%matplotlib notebook

# this is needed to compensate for %matplotlib notebook's tendancy to blow up images when plotted inline

from matplotlib import rcParams

rcParams['figure.autolayout'] = True

%load_ext autoreload

%autoreload 2

With linear regression we aim to fit a line (or hyperplane in higher dimensions) to a scattering of data. In this Section we describe the fundamental concepts underlying this procedure.

Data for regression problems comes in the form of a set of $P$ input/output observation pairs

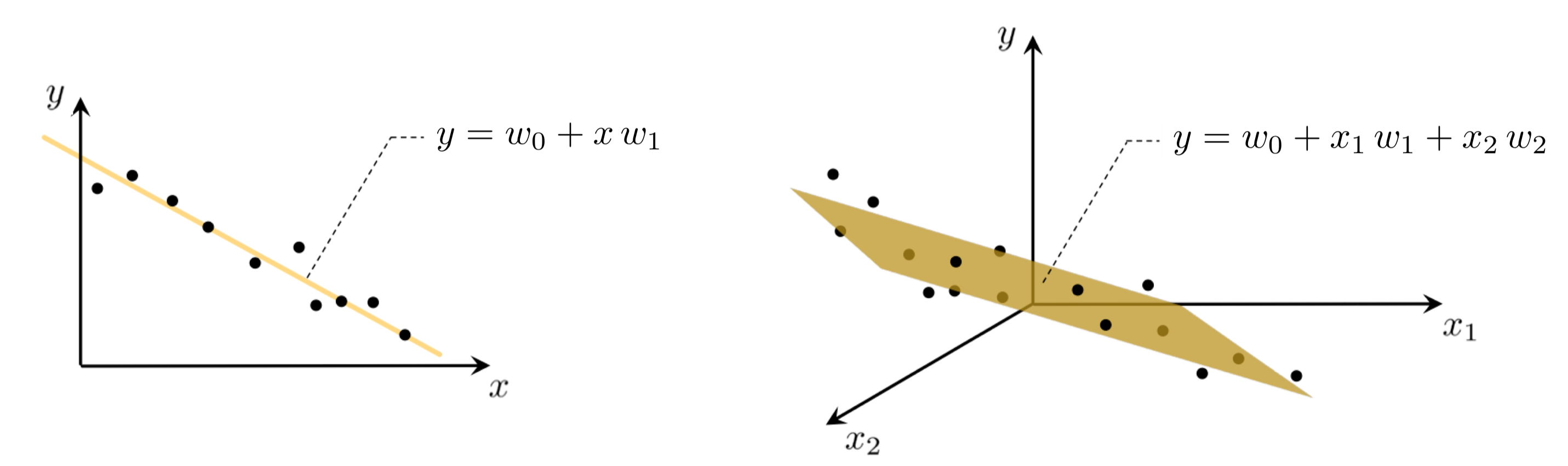

\begin{equation} \left(\mathbf{x}_{1},y_{1}\right),\,\left(\mathbf{x}_{2},y_{2}\right),\,...,\,\left(\mathbf{x}_{P},y_{P}\right) \end{equation}or $\left\{ \left(\mathbf{x}_{p},y_{p}\right)\right\} _{p=1}^{P}$ for short, where $\mathbf{x}_{p}$ and $y_{p}$ denote the $p^{\textrm{th}}$ input and output respectively. In simple instances the input is scalar-valued (the output will always be considered scalar-valued here), and hence the linear regression problem is geometrically speaking one of fitting a line to the associated scatter of data points in 2-dimensional space. In general however each input $\mathbf{x}_{p}$ may be a column vector of length $N$

in which case the linear regression problem is analogously one of fitting a hyperplane to a scatter of points in $N+1$ dimensional space.

In the case of scalar input the fitting of a line to the data requires we determine a vertical intercept $w_0$ and slope $w_1$ so that the following approximate linear relationship holds between the input/output data

\begin{equation} w_{0}+x_{p}w_{1}\approx y_{p},\quad p=1,...,P. \end{equation}Notice that we have used the approximately equal sign because we cannot be sure that all data lies completely on a single line. More generally, when dealing with $N$ dimensional input we have a bias and $N$ associated slope weights to tune properly in order to fit a hyperplane, with the analogous linear relationship written as

\begin{equation} w_{0}+ x_{1,p}w_{1} + x_{2,p}w_{2} + \cdots + x_{N,p}w_{N} \approx y_{p} ,\quad p=1,...,P. \end{equation}For any $N$ we can write the above more compactly by denoting

as

\begin{equation} w_0+\mathbf{x}_{p}^T\mathbf{w} \approx y_{p} ,\quad p=1,...,P. \end{equation}The elements of an input vector $\mathbf{x}_{p}$ are referred to as input features to a regression problem. In the McDonald's revenue history dataset data described in the first post of our basics of mathematical functions series, the input feature was year. Conversely in the GDP growth rate data described in the Example below the first element of the input feature vector might contain the feature unemployment rate (that is, the unemployment data from each country under study), the second might contain the feature education level, and so on.

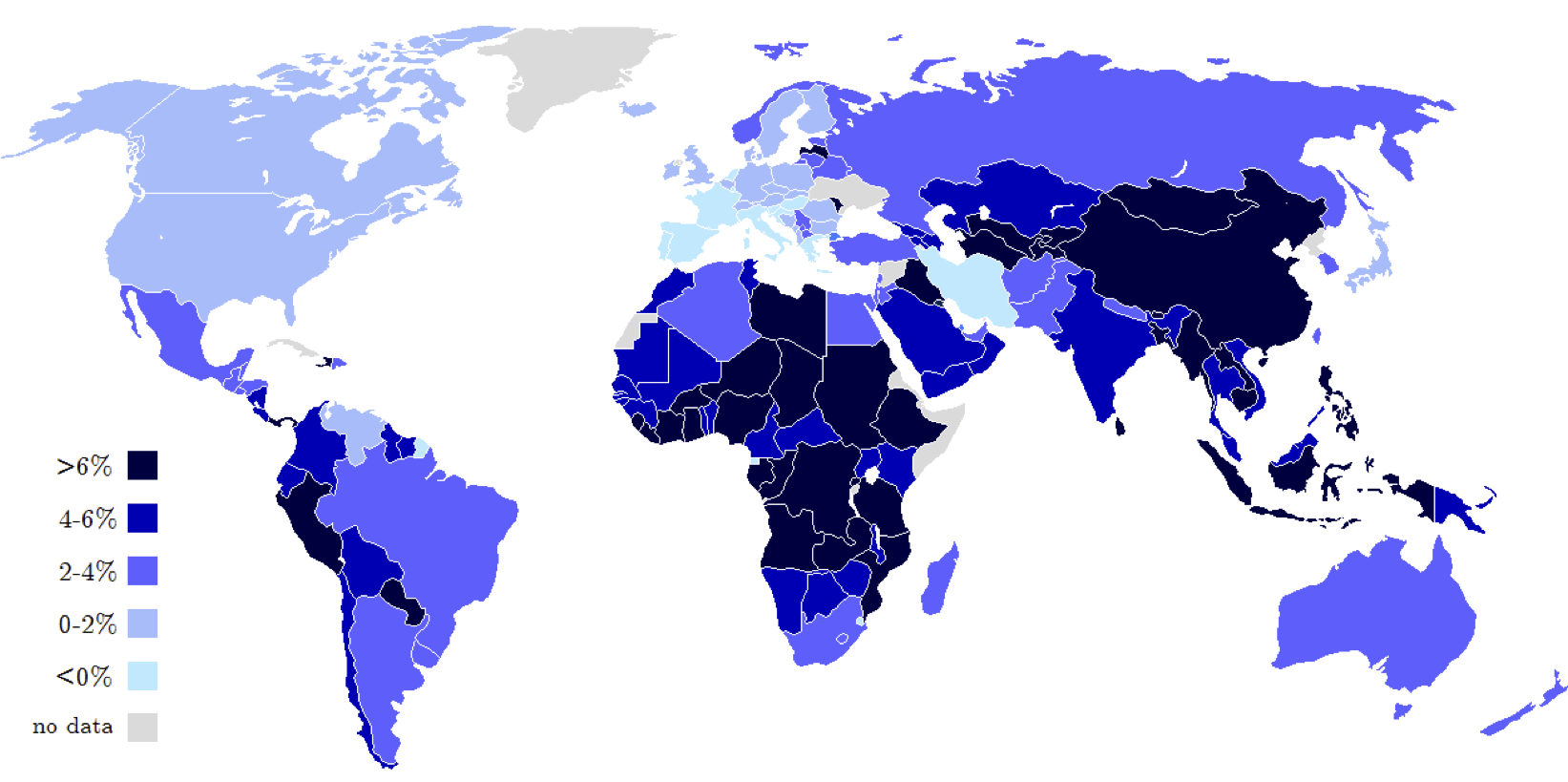

As an example of a regression problem with vector-valued input consider the problem of predicting the growth rate of a country's Gross Domestic Product (GDP), which is the value of all goods and services produced within a country during a single year. Economists are often interested in understanding factors (e.g., unemployment rate, education level, population count, land area, income level, investment rate, life expectancy, etc.,) which determine a country's GDP growth rate in order to inform better financial policy making. To understand how these various features of a country relate to its GDP growth rate economists often perform linear regression.

In the Figure below we show a heat map of the world where countries are color-coded based on their GDP growth rate in 2013, as reported by the International Monetary Fund (IMF).

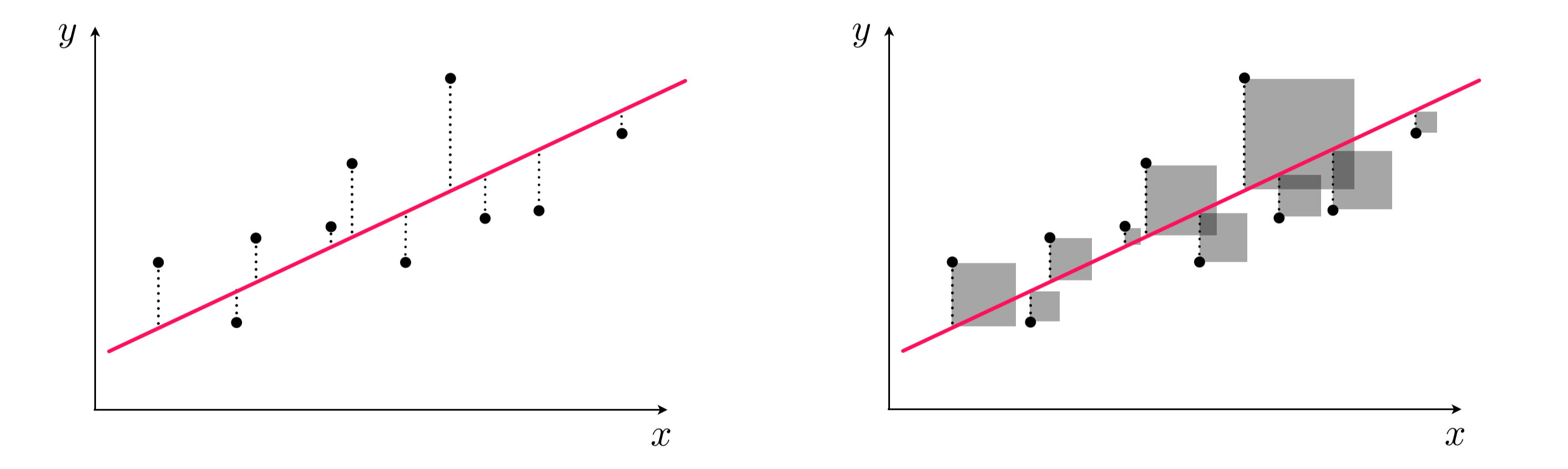

To find the parameters of the hyperplane which best fits a regression dataset, it is common practice to first form the Least Squares cost function. For a given set of parameters $\mathbf{w}$ this cost function computes the total squared error between the associated hyperplane and the data (as illustrated pictorially in the Figure below), giving a good measure of how well the particular linear model fits the dataset. Naturally then the best fitting hyperplane is the one whose parameters minimize this error.

We want to find a weight vector $\mathbf{w}$ and the bias $w_0$ so that each of $P$ approximate equalities

\begin{equation} w_0+\mathbf{x}_{p}^T\mathbf{w} \approx y_{p} \end{equation}holds as well as possible. Another way of stating the above is to say that the error between $w_0+\mathbf{x}_{p}^{T}\mathbf{w}$ and $y_{p}$ is small. One natural way to measure error between two quantities like this is simply to square their difference as

\begin{equation} \left(w_0+\mathbf{x}_{p}^{T}\mathbf{w} - y_{p}^{\,}\right)^2 \end{equation}Since we want all $P$ such values to be small we can sum them up - forming a Least Squares cost function

\begin{equation} \,g\left(w_0,\mathbf{w}\right)=\sum_{p=1}^{P}\left(w_0+\mathbf{x}_{p}^{T}\mathbf{w}-y_{p}^{\,}\right)^{2} \end{equation}for linear regression.

We want to find parameters $w_0$ and $\mathbf{w}$ that provide a small value for $g\left(w_0,\mathbf{w}\right)$ since the larger this value becomes the larger the squared error between the corresponding linear model and the data, and hence the poorer we represent the given dataset using a linear model. In other words, we want to determine a value for the pair $w_0$ and $\mathbf{w}$ that minimizes $g\left(w_0,\mathbf{w}\right)$, or written formally we want to solve the unconstrained problem

As discussed in our mathematical optimization series, generally speaking determining the overall shape of a function - i.e., whether or not a function is convex - helps determine the appropriate optimization method(s) we can apply to efficiently determine the ideal parameters. In the case of the Least Squares cost function for linear regression it is easy to check that the cost function is always convex regardless of the dataset.

For small input dimensions (e.g., $N=1$) we can empirically verify this claim for any given dataset by simply plotting the function $g$ - as a surface and/or contour plot - as we do in the example below.

In this example we plot the contour and surface plot for the Least Squares cost function for linear regression for a toy dataset. This toy dataset consists of 50 points randomly selected off of the line $y = x$, with a small amount of Gaussian noise added to each.

# load in dataset

datapath = '../../mlrefined_datasets/superlearn_datasets/2d_linregress_data.csv'

data = np.asarray(pd.read_csv(datapath,header = None))

# create instance of linear regression demo, used below and in the next examples

demo1 = superlearn.lin_regression_demos.Visualizer(data)

# plot dataset

demo1.plot_data()

The contour plot and corresponding surface generated by the Least Squares cost function using this data are shown below.

# demo.center_data()

demo1.plot_ls_cost(view = [30,80],viewmax = 4,num_contours = 30)

In the previous example we plotted the contour/surface for the Least Squares cost function for linear regression on a specific dataset. There we saw the elliptical contours and 'upward bending' shape of the surface indeed confirms the function's convexity in that case. However the Least Squares cost function for linear regression can mathematically shown to be - in general - a convex function for any dataset. Because of this we can directly apply either gradient descent (and in particular the unnormalized form) or Newton's method in order to minimize it.

The Least Squares cost function for linear regression is always convex regardless of the input dataset, hence we can easily apply either gradient descent or Newton's method in order to minimize it.

The generic practical considerations associated with each method still exist here (see our Mathematical Optimization Series): i.e., with gradient descent we must choose a steplength scheme, and Newton's method is practically limited to cases when $N$ is of moderate value (e.g., in the thousands). For the case of gradient descent we can use a fixed steplength value (and indeed can compute a conservative Lipschitz value that will always produce descent), a diminishing steplength scheme, or an adjustable method like backtracking line search.

The simplest way to code up gradient descent in the same manner as shown above is to simply take the generic unnormalized gradient descent Python code provided in Part 2 of our series on mathematical optimization, and simply plug in the Least Squares cost function. Here the automatic differentiator autograd is used to efficiently compute the gradient at each step. One can implement the cost function in Python as shown in the next Python cell.

# an implementation of the least squares cost function for linear regression for N = 2 input dimension datasets

x = data[:,0] # define input of dataset prior to function definition

y = data[:,1] # define output of dataset prior to function definition

def least_squares(w):

cost = 0

for p in range(0,len(y)):

cost +=(w[0] + w[1]*x[p] - y[p])**2

return cost

Note that because autograd will differentiate with respect to any input to a Python function, officially the only input here can be the weights w. The input/output data x and y should be loaded in prior to defining the function, so that they are included in the scope of the Least Squares implementation, but treated as weights by autograd. Note also that autograd gradient requires input weights be of type autograd.numpy.

Using the implementation above we can evaluate any set of weights we like.

# test out a set of weights using our implementation of the N = 2 least squares function

w = [0,1]

least_squares(w)

To deal with arbitrary input dimension $N$ one then only needs to replace the cost update inside the for loop, i.e., cost +=(w[0] + w[1]*x[p] - y[p])**2, with the more general form.

Alternatively one can 'hard code' the gradient, writing it out algebraically and implementing the same thing in code. Using the more compact notation

\begin{equation} \widetilde{\mathbf{w}}=\left[\begin{array}{c} w_{0}\\ \mathbf{w} \end{array}\right] \,\,\,\,\text{and}\,\,\,\,\, \widetilde{\mathbf{x}}_{p}=\left[\begin{array}{c} 1\\ \mathbf{x}_{p} \end{array}\right] \end{equation}one can easily compute the general form of the gradient by hand (using the derivative rules detailed in our vital elements of calculus series) to be

\begin{equation} \nabla g\left(\widetilde{\mathbf{w}}\right) = 2\sum_{p=1}^{P} \widetilde{\mathbf{x}}_p^{\,}\left(\widetilde{\mathbf{x}}_p^T \widetilde{\mathbf{w}}_{\,}^{\,} - y_p^{\,}\right) \end{equation}In the next Python cell minimize the Least Squares cost using the toy dataset presented in Example 2. In particular since the function is convex we use unnormalized gradient descent, and employ a fixed steplength value $\alpha = 0.01$ for all 75

steps until approximately reaching the minimum of the function. Here we employ the file optimizers.py which contains a short list of optimization algorithms discussed in our series on mathematical optimization, including gradient descent and Newton's method.

# declare an instance of our current our optimizers

opt = superlearn.optimimzers.MyOptimizers()

# run desired algo with initial point, max number of iterations, etc.,

w_hist = opt.gradient_descent(g = least_squares,w = np.asarray([-1.0,-2.0]),max_its = 75,alpha = 10**-2)

Now we animate the process of gradient descent run above. The contour of the cost function is shown in the right panel with each step plotted on top, colored from green at the start of the run to red at its end (green and red points mark the initialization and final weights reached by gradient descent). As you move the slider from left to right the gradient descent process animates, until completion when the slider is all the way to the right. Simultaneously, in the left panel the corresponding linear model given by the weights at each step of gradient descent is drawn. The linear model is colored to match the step of gradient descent, so near the beginning of the run the line is green whereas near the end it is plotted red.

As can be seen while pushing the slider to the right, as the minimum of the cost function is neared, the corresponding weights provide a better and better fit to the data - with the best fit occurring at the end of the run (at the point closest to the minimum).

# animate descent process

demo1.animate_it_2d(w_hist,num_contours = 30)

In Example 6 of our post on Newton's method in our series on mathematical optimization we described how Newton's method perfectly minimizes any quadratic function in a single step. By re-writing it one can show that Least Squares cost function

with any dataset and any $N$, is always a quadratic function, hence Newton's method can be used to minimize it in a single step. Specifically, the cost function can be equivalently rewritten as

where

\begin{equation} \mathbf{A} = \sum_{p=1}^{P}\widetilde{\mathbf{x}}_{p}^{\,} \widetilde{\mathbf{x}}_{p}^T \,\,\,\,\,\,\,\,\,\,\,\,\,\mathbf{b} = -2\sum_{p=1}^{P}\widetilde{\mathbf{x}}_{p}^{\,}y_p^{\,} \,\,\,\,\,\,\,\,\,\,\,\,\, c = \sum_{p=1}^{P}y_p^2 \end{equation}We illustrate the fact that Newton's method can fit a linear regression in a single step below using the same setup as in the previous example, except Newton's method is now used instead of gradient descent. Indeed it takes only a single step to reach the minimum of the cost, while simultaneously finding a set of weights that produces a perfectly fitting line.

# declare an instance of our current our optimizers

opt = superlearn.optimimzers.MyOptimizers()

# run desired algo with initial point, max number of iterations, etc.,

w_hist = opt.newtons_method(g = least_squares,w = np.asarray([-1.0,-2.0]),max_its = 1)

# animate descent process

demo1.animate_it_2d(w_hist,num_contours = 30)

As with gradient descent, one can repeat this experiment by taking the Newton's method code provided in our series on mathematical optimization - which also uses the autograd automatic differentiator - and simply plug in the Python implementation of the Least Squares cost function given in the previous example.

Alternatively if one wishes to write out the Newton step analytically it can be shown to reduce to the following system of linear equations

\begin{equation} \left(\sum_{p=1}^{P} \widetilde{\mathbf{x}}_p^{\,}\widetilde{\mathbf{x}}_p^T \right) \widetilde{\mathbf{w}}_{\,}^{\,} = \sum_{p=1}^{P} \widetilde{\mathbf{x}}_p^{\,} y_p^{\,} \end{equation}In this example we look at another toy dataset with $N = 2$ inputs, which is plotted by the next Python cell. This dataset consists of 50 data points taken randomly from the hyperplane $y = 1 - x_1 - x_2$ with the addition of a small amount of random Gaussian noise to their $y$ value.

# load in dataset

datapath = '../../mlrefined_datasets/superlearn_datasets/3d_linregress_data.csv'

data = np.asarray(pd.read_csv(datapath,header = None))

# create instance of linear regression demo, used below and in the next examples

demo2 = superlearn.lin_regression_demos.Visualizer(data)

# plot dataset

demo2.plot_data()

To fit the Least Squares cost function we must re-define it to accept higher dimensional input. We do this in the next Python cell.

# an implementation of the least squares cost function for linear regression for N = 2 input dimension datasets

x = data[:,:-1] # define input of dataset prior to function definition

y = data[:,-1] # define output of dataset prior to function definition

def least_squares(w):

cost = 0

for p in range(0,len(y)):

x_p = x[p]

y_p = y[p]

a_p = w[0] + sum([a*b for a,b in zip(w[1:],x_p)])

cost +=(a_p - y_p)**2

return cost

In the next Python cell we minimize the Least Squares cost using the unnormalized gradient descent, a constant steplength value $\alpha = 0.001$ for 100 iterations beginning at the point

$$\begin{bmatrix} w_0 \\ w_1 \\ w_2 \end{bmatrix} = \begin{bmatrix} 1 \\ 1 \\ 1 \end{bmatrix}$$# declare an instance of our current our optimizers

opt = superlearn.optimimzers.MyOptimizers()

# run desired algo with initial point, max number of iterations, etc.,

w_hist = opt.gradient_descent(g = least_squares,w = np.asarray([1.0,1.0,1.0]),max_its = 100,alpha = 10**-3)

Now we animate this descent run. Since the linear model in this case has 3 parameters we cannot visualize each step on the contour / surface of the cost function itself, and thus must use a cost function plot (first introduced in our series on mathematical optimization) to keep visual track of the algorithm's progress.

In the left panel below we show the dataset, along with the hyperplane defined by $y = w_0 + x_1w_1 + x_2w_2$ whose weights are given at the current step in the gradient descent run. In the right panel the corresponding cost function value which plots the evaluation of each step up to the current one. Pushing the slider from left to right animates the run from start to finish - updating corresponding hyperplane in the left panel as well as cost function value in the right at each step (both of which simultaneously colored green at the start of the run, and gradually fade to red as the run ends).

As can be seen while pushing the slider to the right, as the minimum of the cost function is neared the corresponding weights provide a better and better fit to the data - with the best fit occurring at the end of the run (at the point closest to the minimum).

# animate descent process

demo2.animate_it_3d(w_hist,view = [10,-40],viewmax = 1.3)

Once we have successfully minimized the Least Squares cost function for linear regression there are a number of ways of measuring the quality of a linear model's fit to the data. If we denote the optimal set of weights found as $w_0^{\star}$ and $\mathbf{w}^{\star}$, then we can compute the average error - commonly called the mean squared error (or MSE) - on the dataset by simply computing the average fit of the model to our dataset as

\begin{equation} \text{MSE}=\frac{1}{P}\sum_{p=1}^{P}\left(w_0^{\star}+\mathbf{x}_{p}^{T}\mathbf{w}^{\star}-y_{p}^{\,}\right)^{2} \end{equation}When possible it is also a good idea to compute the MSE of a learned regression model on a set of new testing data, i.e., data that was not used to learn the model itself, to provide some assurance that the learned model will perform well on future data points. This is explored in further detail in a later post in this Series.

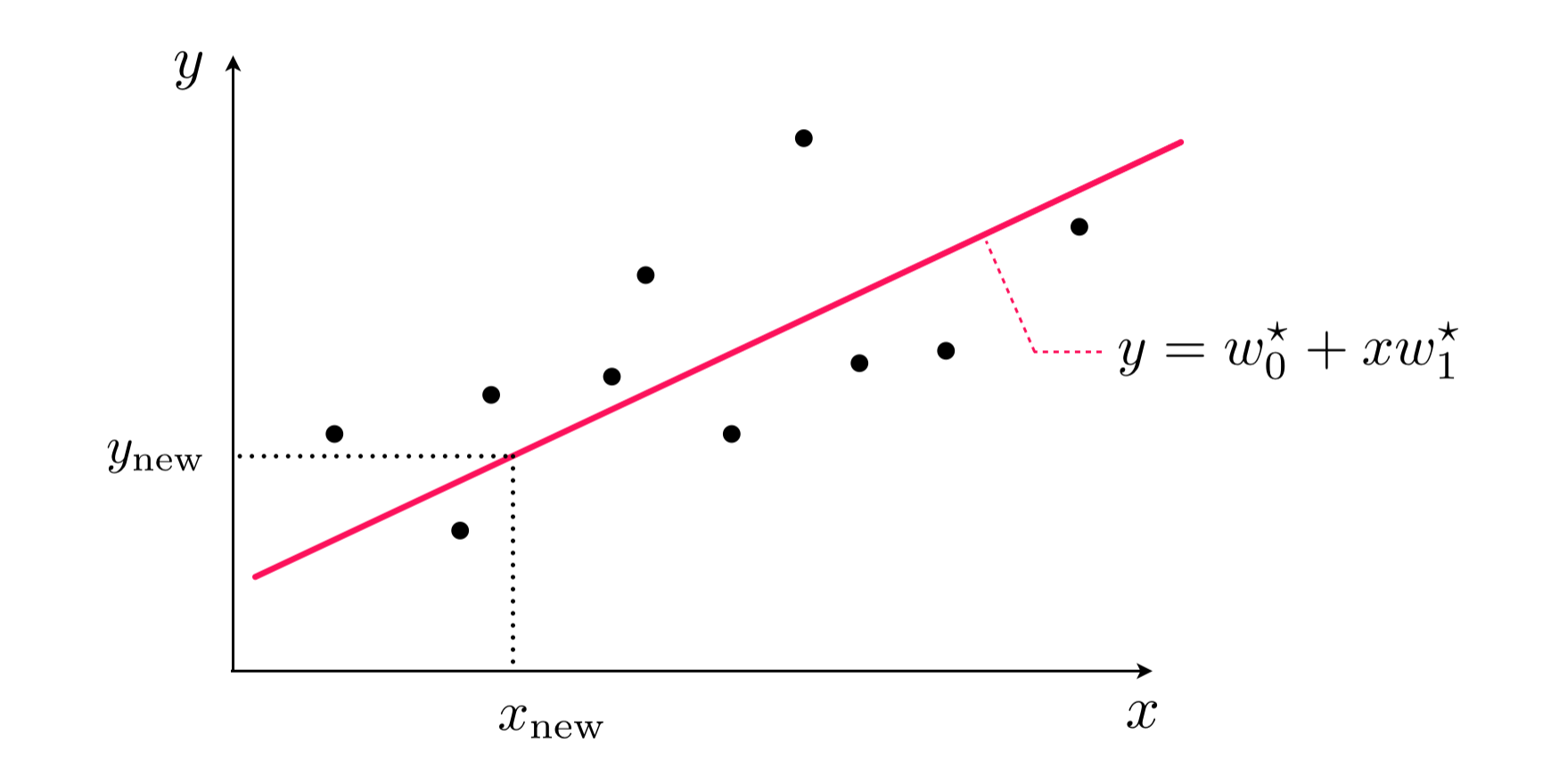

With optimal parameters $w_0^{\star}$ and $\mathbf{w}^{\star}$, found by minimizing the Least Squares cost, we can predict the output $y_{\textrm{new}}$ of a new input feature $\mathbf{x}_{\textrm{new}}$ by simply plugging the new input into the tuned linear model and estimating the associated output as

\begin{equation} y_{\textrm{new}}^{\,}=w_0^{\star}+\mathbf{x}_{\textrm{new}}^{T}\mathbf{w}^{\star} \end{equation}This is illustrated pictorially on a toy dataset for the case when $N=1$ in the Figure below.

As we saw in Subsection 1.1, we built our linear regression model on the fundamental assumption that the relationship between input and output variables is (approximately) linear. That is, we have for all $P$ input/output pairs of data that $w_0+\mathbf{x}_{p}^T\mathbf{w} \approx y_{p}$. Denoting the difference between $y_p$ and $w_0+\mathbf{x}_{p}^T\mathbf{w}$ as $\varepsilon_p$, we can replace these approximate equalities with exact equalities of the form

\begin{equation} w_0+\mathbf{x}_{p}^T\mathbf{w} +\varepsilon_p = y_{p} ,\quad p=1,...,P \end{equation}where $\varepsilon_p$'s can be interpreted as error or noise in the data. With this new notation, the Least Squares cost for linear regression can be written, in terms of $\varepsilon_p$'s, as

\begin{equation} \,g\left(w_0,\mathbf{w}\right) = \sum_{p=1}^{P}\left(w_0^{\,}+\mathbf{x}_{p}^{T}\mathbf{w}^{\,}-y_{p}^{\,}\right)^{2} = \sum_{p=1}^{P} \varepsilon_p^2 \end{equation}Put into words, with linear regression we aim to find the parameters $w_0$ and $\mathbf{w}$ that minimize the total squared noise - a quantity that is referred to as the noise energy in signal processing contexts.

Now one might rightfully ask: what is the point of introducing $P$ new variables $\left\{ \varepsilon_p \right\} _{p=1}^{P}$ to our model when their values are unknown to begin with? While it is true that we do not know the exact $\varepsilon_p$ values, we can nonetheless make assumptions about their distribution that enable us to find $w_0$ and $\mathbf{w}$ (and $\varepsilon_p$'s successively) in a probabilistic framework. Specifically we make the assumption that

1. $\left\{ \varepsilon_p \right\} _{p=1}^{P}$ are drawn from a zero-mean Gaussian distribution. In other words, we assume that the noise is normally distributed with an expected value of $0$. Before getting into why this assumption is necessary to make from a theoretical standpoint, let us examine its validity using a number of real regression datasets.

In the Python cell below we plot both the Least Squares trend line fit to a dataset [1] consisting of satellite measurements of global mean sea level changes on earth from 1993 to 2014 (left panel), as well as the estimated noise distribution according to the learned trend line (right panel).

# load in dataset

datapath = '../../mlrefined_datasets/superlearn_datasets/climate_data.csv'

data = np.asarray(pd.read_csv(datapath,header = None))

demo1 = superlearn.regression_probabilistic_demos.visualizer(data)

# solve Least Squares

demo1.run_algo(algo='newtons_method', w_init = np.random.randn(2,1), max_its = 1)

# visualize results

demo1.error_hist(num_bins=30, xlabel='date', ylabel='sea level', show_pdf='on')

As another example let us look at Francis Galton's height dataset, who collected this data in 1885 in an attempt to explore the relationship between the heights of the parents and the heights of their adult children. In Python cell below we plot the portion of Galton's dataset [2] which connects the height of the mother (input) to the height of her daughter (output), once again plotted along with the error distribution on the right.

# load in dataset

datapath = '../../mlrefined_datasets/superlearn_datasets/mother_daughter.csv'

data = np.asarray(pd.read_csv(datapath,header = None))

demo2 = superlearn.regression_probabilistic_demos.visualizer(data)

# solve Least Squares

demo2.run_algo(algo='newtons_method', w_init = np.random.randn(2,1), max_its = 1)

# visualize results

demo2.error_hist(num_bins = 30, xlabel='height of mother', ylabel='height of daughter', show_pdf='on')

In both cases as you can see it looks like that the noise does follow a zero-mean Gaussian distribution, and hence our assumption is not far-fetched.

Since we have $y_p = w_0+\mathbf{x}_{p}^T\mathbf{w} +\varepsilon_p$ for all $p$, this means that, given the values of $\mathbf{x}_{p}$, $w_0$, and $\mathbf{w}$, each $y_p$ is also Gaussian with the same variance as the noise distribution - which we denote by $\sigma^2$ - and a (shifted) mean value of $w_0+\mathbf{x}_{p}^T\mathbf{w}$. Hence, with our first assumption, we have

\begin{equation} {\cal P}\left(y=y_{p}\,|\,\mathbf{x}_{p},w_0,\mathbf{w}\right)=\frac{1}{\sqrt{2\pi}\,\sigma}e^{\,\frac{-1}{2\sigma^{2}}\left(y-\left(w_0+\mathbf{x}_{p}^{T}\mathbf{w}\right)\right)^{2}} ,\quad p=1,...,P \end{equation}This brings us to the second theoretical assumption we make here, that

2. $\left\{ y_p \right\} _{p=1}^{P}$ are statistically independent of each other. In many cases it makes intuitive sense to assume that our observations are (or can be) made independently of one another other, as long as there is no temporal, spatial, or other kind of correlation in the data.

With these two assumptions we can now form the (joint) likelihood of our data and maximize it to recover model parameters. Specifically, using the independence assumption we can write the likelihood as

\begin{equation} {\cal L}=\prod_{p=1}^{P}{\cal P}\left(y=y_{p}\,|\,\mathbf{x}_{p},w_0,\mathbf{w}\right) \end{equation}Recall, as discussed in our series on the fundamentals of probability and statistics, that maximizing the likelihood is mathematically equivalent to minimizing its negative log-likelihood, giving the probabilistic cost function

\begin{equation} g\left(w_0,\mathbf{w},\sigma\right)=-\sum_{p=1}^{P}\text{log}\,{\cal P}\left(y=y_{p}\,|\,\mathbf{x}_{p},w_0,\mathbf{w}\right) \end{equation}to be minimized over $w_0$, $\mathbf{w}$, and the noise standard deviation $\sigma$.

Our first assumption on the distribution of noise makes it possible to write the exact form of $g$, with some algebra, as

\begin{equation} g\left(\widetilde{\mathbf{w}},\sigma\right)=P\,\text{log}\left(\sqrt{2\pi}\,\sigma\right)+\frac{1}{2\sigma^{2}}\sum_{p=1}^{P} \left(y_p-\widetilde{\mathbf{x}}_{p}^{T}\widetilde{\mathbf{w}}\right)^{2} \end{equation}where we have used the notation

\begin{equation} \widetilde{\mathbf{w}}=\left[\begin{array}{c} w_{0}\\ \mathbf{w} \end{array}\right] \,\,\,\,\text{and}\,\,\,\,\, \widetilde{\mathbf{x}}_{p}=\left[\begin{array}{c} 1\\ \mathbf{x}_{p} \end{array}\right] \end{equation}to write $g$ more compactly.

Checking the first order condition for optimality we have

$$ \begin{array}{c} \nabla_{\widetilde{\mathbf{w}}}g\left(\widetilde{\mathbf{w}},\sigma\right)= \frac{1}{\sigma^{2}}\sum_{p=1}^{P} \mathbf{x}_p\left(y_p-\widetilde{\mathbf{x}}_{p}^{T}\widetilde{\mathbf{w}}\right)=\mathbf{0}\\ \frac{\partial}{\partial\sigma}g\left(\widetilde{\mathbf{w}},\sigma\right)= \frac{P}{\sigma}-\frac{1}{\sigma^{3}}\sum_{p=1}^{P} \left(y_p-\widetilde{\mathbf{x}}_{p}^{T}\widetilde{\mathbf{w}}\right)^{2}=0 \end{array} $$The first equation gives the linear system

\begin{equation} \left(\sum_{p=1}^{P} \widetilde{\mathbf{x}}_p^{\,}\widetilde{\mathbf{x}}_p^T \right) \widetilde{\mathbf{w}}_{\,}^{\,} = \sum_{p=1}^{P} \widetilde{\mathbf{x}}_p^{\,} y_p^{\,} \end{equation}whose solution $\widetilde{\mathbf{w}}^\star$ can be used in the second equation to find the optimal value for the noise variance, as

\begin{equation} \sigma^2 = \frac{1}{P}\sum_{p=1}^{P} \left(y_p-\widetilde{\mathbf{x}}_{p}^{T}\widetilde{\mathbf{w}}^{\star}\right)^{2} \end{equation}Note that the linear system characterizing the fit here is identical to what we derived previously in Subsection 1.3, where interestingly enough, we found the same solution through minimizing the Least Squares cost and without making any of the statistical assumptions made here.

The maximum likelihood solution derived here using the assumptions on noise distribution and independence of data is identical to the Least Squares solution derived previously from a geometric perspective.

Even though it was necessary to assume a Gaussian distribution on the noise in order to re-derive the Least Squares solution from a probabilistic perspective, in practice we can still use Least Squares on datasets where the noise distribution is not necessarily Gaussian.

In the Python cell below we create a simulated dataset with uniformly distributed noise and fit a Least Squares line to it as we did previously in Examples 6 and 7. As you can see, the Least Squares solution still provides a good fit to the data even though the assumption of Gaussian distribution on noise is not met. The right panel here shows the distribution of noise (according to the learned Least Squares fit), which is visibly not Gaussian.

# make and load a simulated dataset with uniformly distributed noise

num_pts = 200

x = np.random.rand(num_pts)

y = 4*x + np.random.rand(num_pts)

x.shape = (len(x),1)

y.shape = (len(y),1)

data = np.concatenate((x,y),axis = 1)

demo3 = superlearn.regression_probabilistic_demos.visualizer(data)

# solve Least Squares

demo3.run_algo(algo='newtons_method', w_init = np.random.randn(2,1), max_its = 1)

# visualize results

demo3.error_hist(num_bins = 30)

In this brief Section we provide derivations which (i) confirm that the Least Squares cost function for linear regression is always convex and (ii) compute its analytical Lipschitz constant. As detailed in our series on mathematical optimization the latter value provides a conservative lower bound on the magnitude of fixed steplength values one should try out with gradient descent.

To show that the Least Squares cost function for linear regression is convex we can use the fact that it is a quadratic as indicated in Example 4 above. There we mentioned that, when written in quadratic form, the matrix generating the corresponding quadratic can be written as $\mathbf{A} = \sum_{p=1}^{P}\widetilde{\mathbf{x}}_p^{\,}\widetilde{\mathbf{x}}_p^T$. From our post on quadratic functions and eigenvalues in our series on the vital elements of calculus, to show that this quadratic is convex we can just show that the eigenvalues of this matrix are all nonnegative. Furthermore, we know that the smallest eigenvalue of any square symmetric matrix $\mathbf{A}$ is given as the minimum of the Rayleigh quotient (as detailed in our post on unconstrained optimality conditions in the vital elements of calculus series), i.e., the smallest value taken by

\begin{equation} \widetilde{\mathbf{w}}^T \mathbf{A} \widetilde{\mathbf{w}}^{\,} \end{equation}for any unit-length vector $\widetilde{\mathbf{w}}$. Substituting in the particular form of $\mathbf{A}$ here we have

\begin{equation} \widetilde{\mathbf{w}}^T\left(\sum_{p=1}^{P}\widetilde{\mathbf{x}}_p^{\,}\widetilde{\mathbf{x}}_p^T \right) \widetilde{\mathbf{w}}^{\,} = \sum_{p=1}^{P}\left(\widetilde{\mathbf{w}}^T\widetilde{\mathbf{x}}_{p}^{\,}\right)\left( \widetilde{\mathbf{x}}_{p}^T \widetilde{\mathbf{w}}^{\,} \right) = \sum_{p=1}^{P}\left(\widetilde{\mathbf{w}}^T\widetilde{\mathbf{x}}_{p}^{\,}\right)^2 \end{equation}Since each term in the summand is squared, the sum must be nonnegative. Therefore the minimum eigenvalue of the Least Squares cost (quadratic) function is nonnegative, and it is therefore convex.

Since we have just seen that the cost function is convex in order to compute a Lipschitz constant we can simply compute the largest eigenvalue of the matrix $\mathbf{A} = \sum_{p=1}^{P}\widetilde{\mathbf{x}}_p^{\,}\widetilde{\mathbf{x}}_p^T$. This is precisely given as the 2-norm of this matrix, squared

\begin{equation} L = \left\Vert \sum_{p=1}^{P}\widetilde{\mathbf{x}}_p^{\,}\widetilde{\mathbf{x}}_p^T\right\Vert_2^2 \end{equation}which one can compute via e.g., the power method.

For a larger but easier to compute Lipschitz constant one can use the trace of the matrix $\mathbf{A}$, since this equals the sum of all eigenvalues, which in this case must be larger than its maximum value since all eigenvalues are non-negative.

[1] RS Nerem, DP Chambers, C Choe, and GT Mitchum. Estimating mean sea level change from the topex and jason altimeter missions. Marine Geodesy, 33(S1):435–446, 2010.

[2] Data taken from https://www.statcrunch.com/5.0/shareddata.php?keywords=Galton